WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors

– Gold expected to build on 2017 gains into 2018 despite headwind conditions

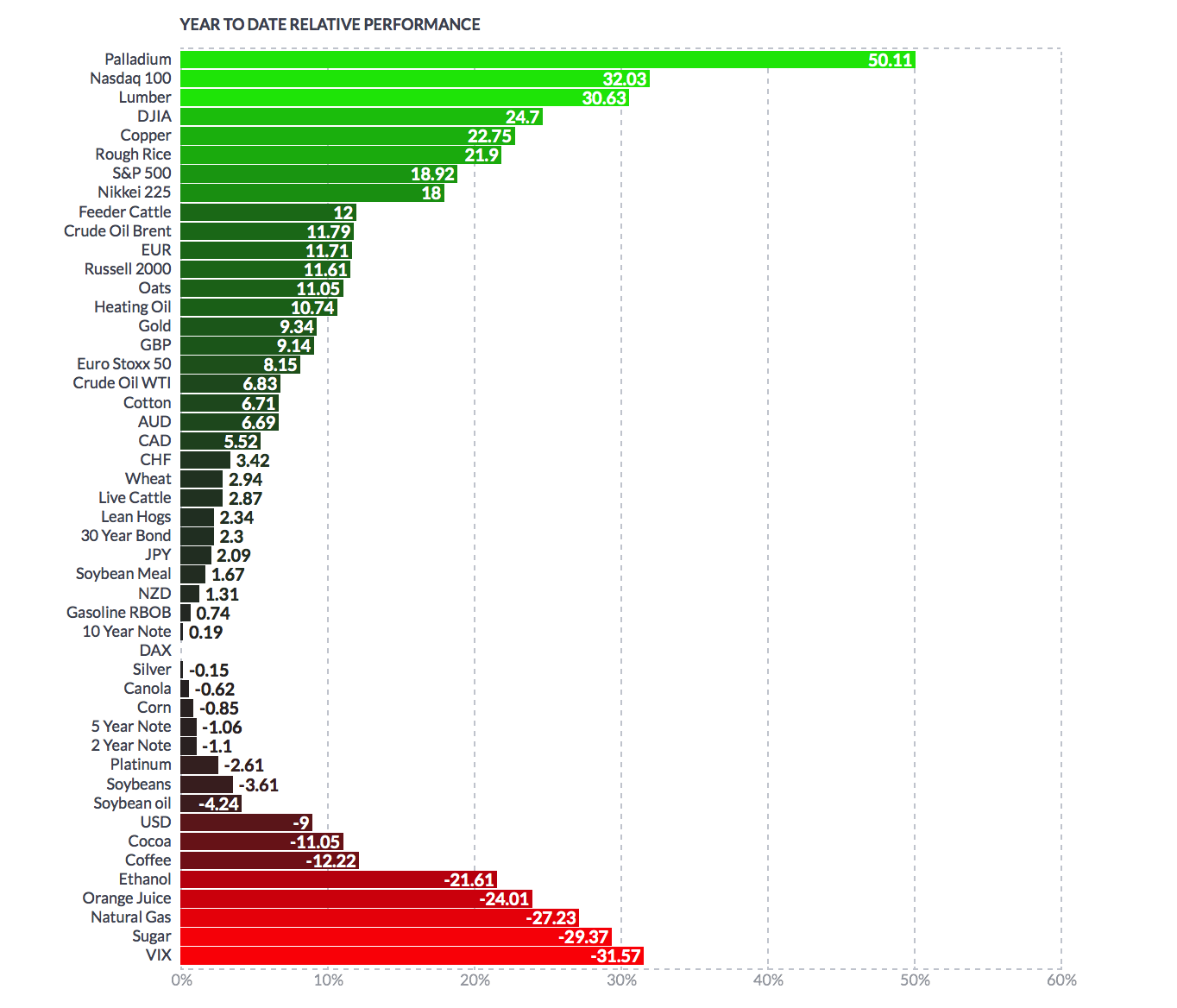

– Gold has gained more than 9% in the year-to-date

– Monetary policy and policymakers will continue to be “significant drivers of gold demand”

– Physical and structural market changes will support gold into 2018

– Goldcore has been at forefront of reporting on major developments in gold market and price

Gold’s had a tough year. This isn’t in reference to price. After all, it has made double-digit gains in some currencies and US Gold futures are up more than 9%. The precious metal has had some harsh criticism from the mainstream media and unfair comparisons to bubblicious assets, such as bitcoin and US equities.

Few have acknowledged gold’s impressive performance in the face of rising interest rates, tightening monetary policies and the ongoing equity bull market.

The World Gold Council’s Chief Market Strategist John Reade is optimistic that gold can carry on with its strong performance, well into 2018. Below, we outline how he expects gold to perform next year.

Monetary policy and Fed chairs

Monetary policy – and policymakers – will continue to be significant drivers of gold demand, given that the Federal Reserve (the Fed) is anticipated by many to hike rates further next year and start to allow its balance sheet to contract. The new staff roster may also change the way the Fed acts and communicates. Jerome Powell, nominated as the next Fed chair, recently aired his views on Fed communications and any changes that he makes could lead to a period of adjustment by fixed income and other markets. Other staff will change too, most interestingly the suggestion that Mohamed El-Erian – a known supporter of gold as an investment asset – may become vice-chairman.

Jerome Powell will certainly be one to watch in the coming months. As we explained yesterday Janet Yellen is considered to have been successful in navigating the US economy. Powell is unlikely to rock the boat too much in the eyes of the FOMC but this does not necessarily mean great things for the global economy.

You can read more about the likely new Fed Chair Jerome Powell and our thoughts on what he will (or won’t) bring to the table.

Not just the Fed feeding the gold price

Of course, it is not all about the US central bank. Over the next 12 months, we may see a slowdown in the ECB’s extraordinary monetary policy action, while even the Bank of Japan may dial back its quantitative easing. Finally, China could continue its efforts to rebalance economic growth and possibly de-leverage some sectors of the economy.

Not only are central banks ones to watch when it comes to monetary policy but also when it comes to their influence on banking rules. This was something we’ve covered a lot this year, with the ECB’s proposal to end deposit protection as one of the most important stories of the year. It served as a timely reminder as to why keeping assets out of the banking system was more pertinent than ever.

This week we’ve had a rally of central bank announcements. The FOMC increased rates by 0.25% whilst the Bank of England maintained at 0.5%. Both decisions were influenced by inflation rates. For the US, inflation remains ‘stubbornly’ low, whilst in the UK Mark Carney has been forced to explain the above target rate of 3.1%.

With inflation still subdued around the world, we see monetary policy tightening as likely to be gentle, but there are risks, not least the Fed’s planned balance sheet reduction – the first time such an action has been attempted.

Read more: Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

Gold to benefit from US dollar headwind

Away from monetary policy, we view two other factors as potentially important for gold. First, the ongoing strength – or otherwise – of already expensive US equities. And second, the trajectory of the US dollar. We believe that the bull market in US equities has reduced gold’s appeal in 2017: an end to that trend could reignite demand for gold. The direction of the US dollar could also be important: if 2017 marks the end of a multi-year period of US dollar strength, gold could benefit from that tailwind, unlike the headwind that it has experienced since 2001.

When it comes to the US dollar strength various charts should not be considered as the only way to read the market. We’ve paid a lot of attention this year towards the ongoing move away from US dollar hegemony.

From Russia to China to Venezuela support for the currency is rapidly depreciating. Much of this is thanks to countries establishing trading mechanisms that embrace the borderless and sovereign-free currency of gold bullion.

Read more: Own Gold Bullion To “Support National Security” – Russian Central Bank

Positives in the Physical Market

What physical market trends should investors pay attention to in 2018? Income growth is probably the most significant because, over the long run, it has been the most important driver of gold demand. And we believe the outlook here is encouraging. China, the world’s largest gold market, has avoided the hard landing that many were predicting 18 months ago and is expected to grow at a fair clip in 2018, with the consensus forecast at around 6.4%.

The Indian economy is recovering from the shock demonetisation of 2016 and adjusting to the Goods and Service Tax rolled out in 2017. The slowdown in GDP growth last year is expected to moderate, as businesses and consumers adapt. Indeed, India is expected to be one of the fastest-growing countries in the world in 2018, expanding at an even faster rate than it did between 2012-2014.

Stories of strong demand in India and China are usually expected at various times in the year. What no one in the mainstream was prepared for in 2017 was the decade-long evidence that Germans had been boosting their personal gold reserves.

Solid income growth in the world’s largest gold markets would undoubtedly be viewed as good news. But other countries are making progress too. Germany’s economy is expected to maintain its momentum and unemployment is anticipated to continue falling, providing support for the world’s third-largest bar and coin market. Across the Atlantic, the US jewellery market, the third-largest in the world, could benefit from continuing economic growth and high consumer confidence.

Read more: Geopolitical Risk Highest “In Four Decades” – Gold Demand in Germany and Globally to Remain Robust

Structural changes in the gold market are also worth noting. These may not have a direct impact on the gold market in 2018, but they can herald significant changes in the years to come. Potential changes to the VAT rate currently applied to gold bars in Russia is a case in point. A punitive 18% has stifled market growth, so a reduction could open up an exciting new market. Elsewhere, banks and mints are continuing to develop Shari’ah-compliant gold products, and we may see this part of the market gain traction. And in India, the move to develop a spot exchange could result in greater transparency, boosting India’s gold trade.

Read more about Shari’ah-compliant gold products here.

News and Commentary

Gold steady amid subdued dollar, poised for weekly gain (Reuters.com)

Dollar Eyes Weekly Drop on Tax; Asia Stocks Fall (Bloomberg.com)

U.S. regulators ditch net neutrality rules as legal battles loom (Reuters.com)

Gold will continue its climb in 2018, World Gold Council predicts (MarketWatch.com)

ref: finviz

World’s Biggest Pension Fund Says AI Will Replace Asset Managers (Bloomberg.com)

New York Fed Inflation Gauge And Gold Price (Gold-Eagle.com)

Central Banks Want the World to Carry On While They Quietly Tighten (Bloomberg.com)

Crypto Vs. Gold: Gold Has Value Unto Itself (SeekingAlpha.com)

What the World’s Central Banks Are Saying About Bitcoin (Bloomberg.com)

Gold Prices (LBMA AM)

15 Dec: USD 1,257.25, GBP 937.41 & EUR 1,065.52 per ounce

14 Dec: USD 1,255.60, GBP 935.67 & EUR 1,062.49 per ounce

13 Dec: USD 1,241.60, GBP 929.96 & EUR 1,056.97 per ounce

12 Dec: USD 1,243.40, GBP 933.92 & EUR 1,056.27 per ounce

11 Dec: USD 1,251.40, GBP 935.80 & EUR 1,061.19 per ounce

08 Dec: USD 1,245.85, GBP 924.42 & EUR 1,061.09 per ounce

07 Dec: USD 1,256.80, GBP 937.57 & EUR 1,066.77 per ounce

Silver Prices (LBMA)

15 Dec: USD 15.99, GBP 11.93 & EUR 13.55 per ounce

14 Dec: USD 16.01, GBP 11.92 & EUR 13.54 per ounce

13 Dec: USD 15.71, GBP 11.76 & EUR 13.38 per ounce

12 Dec: USD 15.78, GBP 11.82 & EUR 13.40 per ounce

11 Dec: USD 15.84, GBP 11.84 & EUR 13.43 per ounce

08 Dec: USD 15.83, GBP 11.76 & EUR 13.48 per ounce

07 Dec: USD 15.91, GBP 11.94 & EUR 13.49 per ounce

Recent Market Updates

– Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

– UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

– An Interview with GoldCore Founder, Mark O’Byrne

– Low Cost Gold In The Age Of QE, AI, Trump and War

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

Important Guides

For your perusal, below are our most popular guides in 2017:

Essential Guide To Storing Gold In Switzerland

Essential Guide To Storing Gold In Singapore

Essential Guide to Tax Free Gold Sovereigns (UK)

Please share our research with family, friends and colleagues who you think would benefit from being informed by it.

The post WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors appeared first on GoldCore Gold Bullion Dealer.

![]()

Leave A Comment

You must be logged in to post a comment.