We could be heading for a golden age – or a return to the 1970s

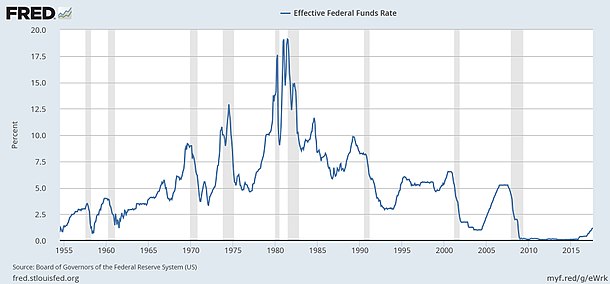

The cost to the US government of borrowing money for a decade came within sniffing distance of 3% yesterday.

The US ten-year Treasury yield is sitting at 2.96% as I write this morning, having got to 2.99% yesterday.

Does this really matter? After all, 3% is just another number.

On the one hand, you’d be right to think that. On the other, it’s not so much the number as the direction that’s significant.

What the end of the bond bull market implies

If the US ten-year Treasury yield does breach 3%, we’ll be at heady heights not seen since 2013.

The big issue here is that bonds have been in a bull market since the early 1980s. In other words, yields (interest rates) have been falling, and bond prices have been rising.

This bull market in bonds has been accompanied by an almost equally long-lived bull market in equities. Stocks have suffered more painful crashes along the way, but broadly speaking, we had almost 20 years of good times up to 2000, then a crash to 2003, a rebound to 2007, another crash to 2009, and then near-enough another decade of good times.

So the question now is: if bond yields are really turning up now (having reached unprecedentedly low levels), then what does that imply for everything else?

After all, as bond yields have gone down, pretty much everything else has gone up. That’s logical. When bond yields are at 10%, a property that rents at an annual yield of around 12% is not very appealing. When bond yields fall to 5%, suddenly that property looks a lot more attractive. As a result, more money flows into property (say) and prices there go up (driving yields down).

That’s the basic mechanism at work here. So that, in turn, implies that if bond yields go up, then yields on everything else have to go up too. And rising yields on most assets (bonds mostly pay a fixed income) imply that either prices have to fall or profits have to rise (or both).

For example, if I own a property with a rental yield of 5% and I can get 8% from a risk-free government bond, then one of two things is going to happen: either I push the rent up so that I’m earning a better yield, or the market value of my property is going to slide sharply.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Or if I own a share that yields 5%, and I can get 8% from a government bond, I’ll either want to see management raise the dividend payout, or at least demonstrate that profitability has risen in such a way that a higher dividend could be funded; or the share price will fall to reflect the fact that you’re getting a better reward for taking less risk elsewhere.

So what does this mean?

What we want is some “good inflation”

The only real way to get sustained improvements in profitability is via productivity gains – doing more with the same, or fewer, resources. So if we’re going to get a productivity boom, then we can cope with higher interest rates and still enjoy decent investment returns.

In this case, rising inflation implies that we are reaching the limits of what we can currently get out of the resources that are being used. The idea is that companies (mainly) then invest to increase productivity and efficiency, and things improve.

So if inflation rises because you’ve got healthy growth which is driving higher demand, then it’s not so bad. Rising borrowing costs might cause problems for over-leveraged companies and individuals. But as long as the broader economic strength is there, then while there will be a few potholes in the road, it’s hard to complain.

It’s true that stocks tend not to like it when inflation starts to risk getting out of hand – maybe around the 4% mark. By that time, central banks are taking notice and perhaps raising short-term borrowing costs, and eventually bringing the whole thing to a grinding halt, as everyone who over-leveraged themselves in the boom suddenly has to cough up money they don’t have.

However, that’s still a problem for tomorrow. Particularly if the Federal Reserve and other central banks (as I suspect) wouldn’t mind a wee bit of inflation to take the edge off the huge debts we’ve built up in recent years.

What you don’t want is “bad inflation”

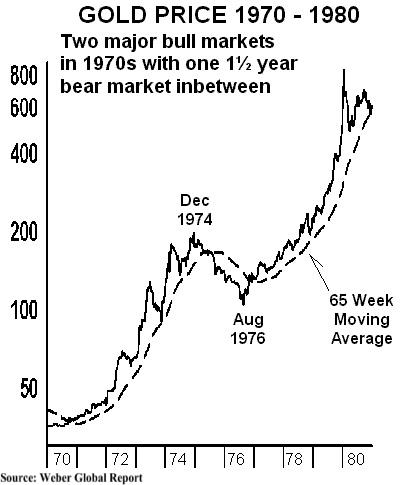

What you really don’t want though, is “stagflation”. That’s where you get rising raw material costs, accompanied by weak or non-existent economic growth. That’s what characterised the 1970s, and it really wasn’t fun for investors.

This is the sort of environment that could be brought on by global trade wars, say. It becomes harder and more to do business with one another, and it also becomes harder and more expensive to secure the supplies of raw materials that everyone needs. Sales fall, costs rise – that’s a nasty combination.

In a way, stagflation is what you get when an economy becomes less productive. Prices are rising at the same time as efficiency is deteriorating.

Between a golden age and the 1970s

So, getting back to the point in hand, what does the 3% mark portend?

There are three main options. The US Treasury bumps its head against the 3% mark again, falls back down, and we get a recession before any of this can become an issue. We fall back into the deflationary pit. I think that’s unlikely.

The other option is that yields rise above 3% and it’s OK because we’re embarking on a world where productivity will improve. Technology leads us to the sunny uplands where workers and robots working together in harmony creates a more efficient, more profitable workplace, and companies make more profits, and everyone gets higher pay rises, and inflation rises just enough to take the edge off our debts but not enough to make us all miserable. A new golden age.

That sounds nice.

The final option is that yields go above 3% because commodity prices are rising fast. They’re rising fast because globalisation is being unwound. Wages start rising too – but not because companies have more profits, instead it’s because voters are fed up with slow-rising wages and fast-rising asset prices. So asset prices crash and certain groups of workers (the most politically sensitive) get pay hikes, while those on the margins get laid off.

That’s your “return to the 1970s” scenario.

Conclusion

I’m hoping for the golden age. But I’m preparing for the less enjoyable option. My advice on what it means for your portfolio stays the same.

Avoid what’s overvalued. And own some gold.

Money Week have a free daily investment email called Money Morning. Sign up here

GoldCore Editors Note: Given the scale of debt in the global financial system and threatening the global economy, we see stagflation as increasingly likely. In that scenario, gold will likely outperform most assets as it did in the 1970s when it rose 2,300% in just nine years.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

News and Commentary

Gold prices steady ahead of U.S. payrolls data (Reuters.com)

Asia Stocks Drop as Trade Talks Held; Dollar Slips (Bloomberg.com)

U.S. Trade Gap Narrows, Claims Remain Low, Productivity Tepid (Bloomberg.com)

U.S. factory orders rise, but business equipment spending slowing (Reuters.com)

ISM non-manufacturing index slows to four-month low in April (MarketWatch.com)

Don’t Be Afraid Of Fed, Gold Price To Touch $1,600 (Forbes.com)

PREPARING FOR A RECESSION (RealVision.com)

Has the Fed really turned hawkish? Or is it just an act? (MoneyWeek.com)

Global RESET Challenge: Ultimate Twist (GoldSeek.com)

Jeffrey Gundlach: Gold to explode (MoneyWeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

03 May: USD 1,313.30, GBP 966.19 & EUR 1,094.64 per ounce

02 May: USD 1,310.75, GBP 960.52 & EUR 1,091.99 per ounce

01 May: USD 1,309.20, GBP 956.37 & EUR 1,087.68 per ounce

30 Apr: USD 1,316.25, GBP 958.62 & EUR 1,087.62 per ounce

27 Apr: USD 1,317.70, GBP 954.41 & EUR 1,090.79 per ounce

26 Apr: USD 1,321.90, GBP 949.52 & EUR 1,085.94 per ounce

25 Apr: USD 1,325.70, GBP 949.47 & EUR 1,085.48 per ounce

Silver Prices (LBMA)

03 May: USD 16.47, GBP 12.12 & EUR 13.74 per ounce

02 May: USD 16.35, GBP 11.98 & EUR 13.62 per ounce

01 May: USD 16.25, GBP 11.87 & EUR 13.51 per ounce

30 Apr: USD 16.38, GBP 11.93 & EUR 13.54 per ounce

27 Apr: USD 16.53, GBP 12.01 & EUR 13.68 per ounce

26 Apr: USD 16.58, GBP 11.87 & EUR 13.61 per ounce

25 Apr: USD 16.57, GBP 11.87 & EUR 13.57 per ounce

Recent Market Updates

– Smart Money Diversifying Into Gold – One Billionaire Invests Half His Net Worth

– “Blood In The Streets” Of U.S. Gold Bullion Market As Sale Of Gold Coins Collapse

– Most Important Chart Of The Century For Investors?

– Gold Mining Shares Are Speculative Making Gold Bullion A Better Investment

– Gold Price Increasingly Influenced By Declining Dollar Rather Than Interest Rates

– Cash “Vanishes” From Bank Accounts In Ireland

– Russia Buys 300,000 Ounces Of Gold In March – Nears 2,000 Tons In Gold Reserves

– Family Offices and HNWs Invest In Gold Again

– New All Time Record Highs For Gold In 2019

– Palladium Bullion Surges 17% In 9 Days On Russian Supply Concerns

– Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

The post Own Some Gold and Avoid Overvalued Assets appeared first on GoldCore Gold Bullion Dealer.

![]()

Leave A Comment

You must be logged in to post a comment.