– London property market tumbles as glut of luxury apartments grows to 3,000

– Property crisis in London as over half of 1,900 luxury apartments built 2017 fail to sell

– London’s still high priced property causes companies to locate offices elsewhere

– At current rates, glut of London properties will take three years to sell

– Leading London-based estate agents Foxtons’ sees 42% drop in earnings, yoy

– UK’s largest estate agent issues second profit warning in three months

– Number of homes sold in December fell to 99,100, lowest level since Nov 2016

– The ‘Shard disaster’ – Ten apartments at top of London’s largest skyscraper, all priced over £50m and in five years not a single one has sold

– Property gold? Diversify and own the physical property of real gold

Editor: Mark O’Byrne

There is much talk of bubbles bursting of late. Bitcoin, bonds have been considered in this regard but so far very little consideration of the property bubbles in London, Sydney, Toronto, Vancouver, Hong Long and other major cities.

London’s property market is another market to consider when looking for evidence that the party is over when it comes to frothy, record-high asset prices.

On average, UK properties take around six weeks to sell. London properties have been consistently below average, with many taking less than a day to go from ‘For Sale’ to ‘Under Offer’. However, in recent months, three London regions – West, North-West and South-West – appeared in the slowest 10 postcode areas for property sales.

According to this research by the Homeowners Alliance, West London has taken the very bottom spot after properties spent an average of 107.9 days on the market as of last month.

This is in line with other data that shows property prices in the capital have fallen for the first time since 2009.

Delicate buyers: London becomes price-sensitive

One of the first things someone outside of London says about the city is how expensive it is. They often say it as if those of us who are from there have never noticed.

Arguably, this has been the case for the last eight years or so when it comes to London’s luxury properties. But it seems many buyers are waking up to the sheer madness of paying millions for a tiny shoe box small apartment, that is in the no man’s land of Brexit and majorly exposed to the vulnerable indebted UK economy and a further devaluation of the pound.

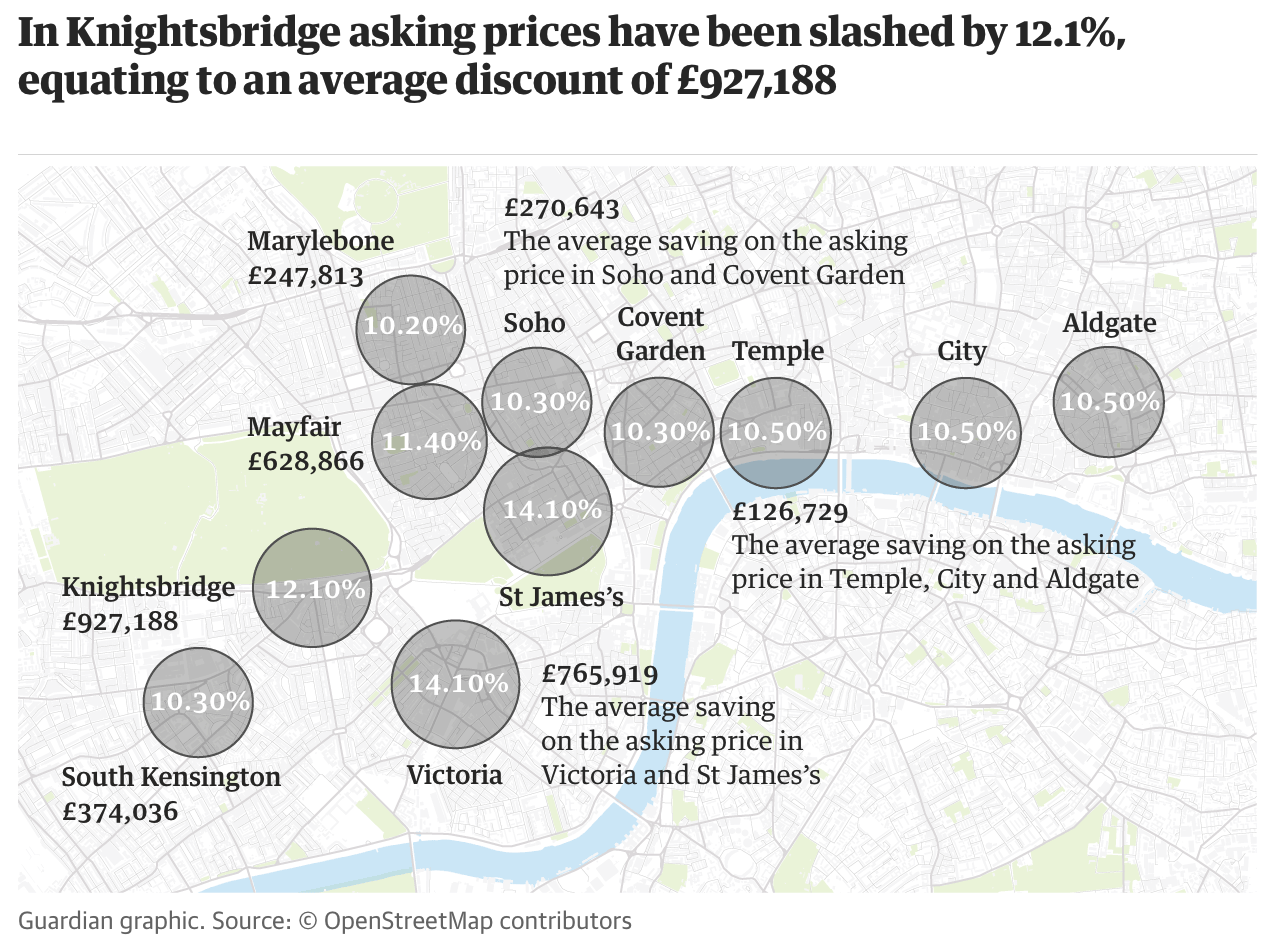

The Guardian reports that more than half of the 1,900 ultra-luxury apartments built in London last year failed to shift. There are now an estimated 3,000 unsold luxury properties, such as these, in the capital. These are the apartments that are priced above £1,500 per square-foot.

For the slightly cheaper apartments, priced at between £1,000-£1,500 per sq ft, there are 14,000 unsold properties. The average price per sq ft across the country is £211.

In the West of London (the worst performing area in the UK in terms of days sold) Savills is marketing a two-bedroom duplex penthouse for £7.25m, a ridiculous amount. But, this is not as eye watering when you consider it has already had a discount of 39.6 per cent off its original launch price of £12m.

“76 per cent of properties have been on the market for more than six months [In St. James’s]” says Tim Macpherson, head of London residential sales at Carter Jonas, and “almost half – 45.7 per cent – have been reduced in price”.

The problem really is very serious in the West of London. The Guardian reports:

The steepest discounts are currently to be found in St James’s and Victoria, where the average prime property price has been reduced by 14.1% (£766,000) and where more than three-quarters of homes have been on the market for more than six months. In Knightsbridge, prices have been reduced by 12.1% on average, followed by Mayfair (11.4%) and Temple and the City (10.5%).

Gluttonous property developers of London

In any other industry a glut of supply would require the manufacturers to take stock of what was going on and likely hold off on producing any more goods until the glut had shifted or a new strategy had been taken. This would be forced to happen in any industry where the environmental and social disruption was so great, thanks to the production process.

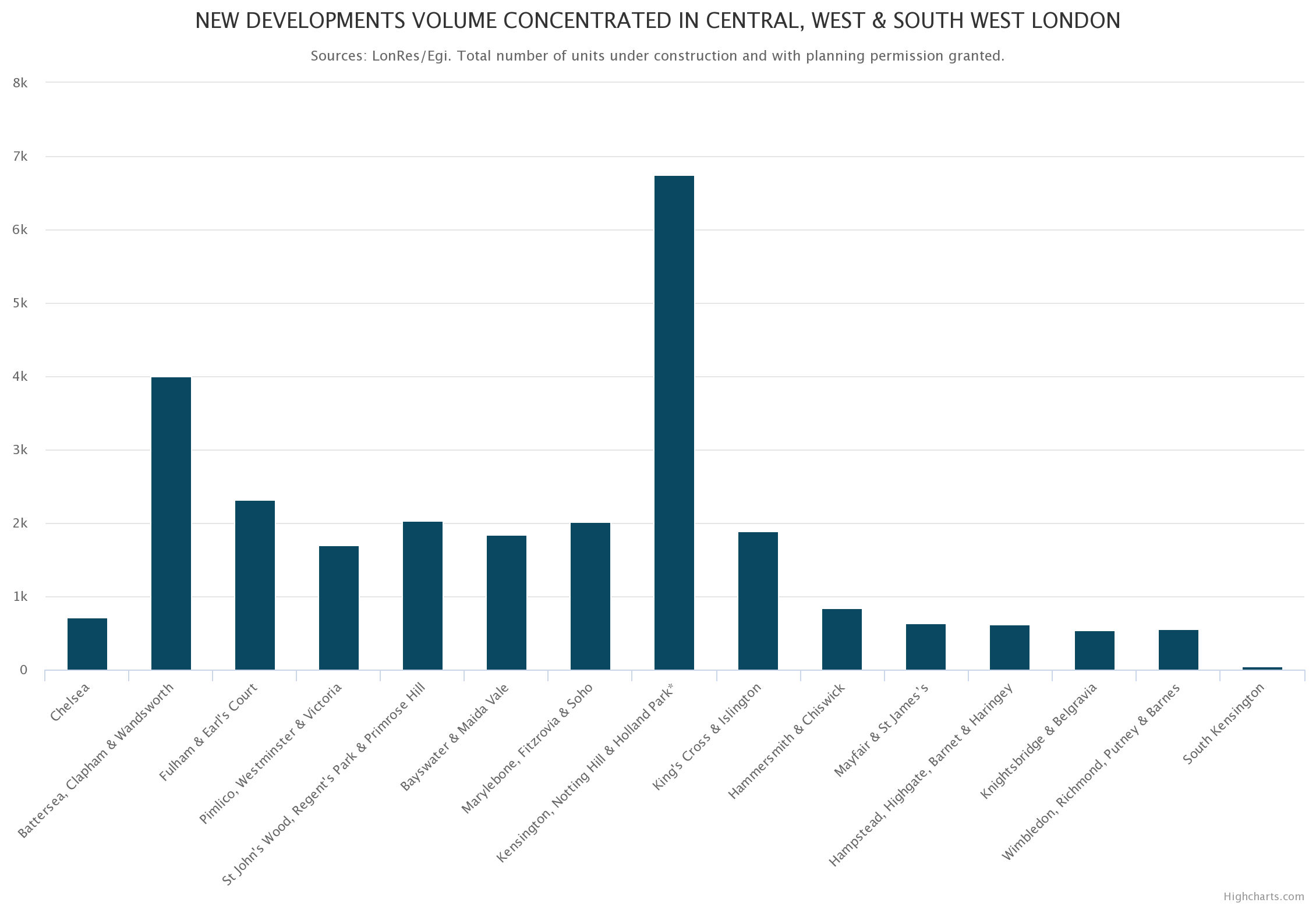

But not in London. No authority has stepped in and demanded building firms halt works. Instead, there are a further 420 residential towers (each at least 20 storeys high) in the pipeline, according to New London Architecture and GL Hearn.

The Coutts London Prime Property Index Q4 2017, warns of the risk of ‘over supply’:

Londoners have grown used to the sight of cranes and construction sites dotted across the capital. More than 26,000 new units are currently under construction or have received permission to start building in post codes covered by the Coutts London Prime Property Index as at December 2017.

New developments are cropping up throughout the 15 areas we cover, but it’s Central and West & South West London that are leading the charge. While this reflects the degree of demand in these sought-after areas, there is a risk of a potential over-supply of luxury new builds leading to an increase in listing times for them and higher discounts than on existing homes.

The government love this. They believe that this promotes confidence in the capital. They are happy with this – especially at a time when financial companies are threatening to pull out jobs and offices in the City, in the face of Brexit. For some reason, building more residential apartments means we don’t need to worry about it. But who is going to buy them?

Not the foreigners we have so long relied on, it seems. Property buying agent Henry Pryor told the Guardian:

“We’re going to have loads of empty and part-built posh ghost towers,” he says. “They were built as gambling chips for rich overseas investors, but they are no longer interested in the London casino and have moved on.”

So the London Casino’s chips are down, the house has folded. But the owners keep building more roulette tables and penthouses, desperate to try and entice the gamblers. Where was the tipping point? Most likely London’s very own phallic-symbol of arrogance, the Shard.

There are ten apartments at the top of the capital’s largest skyscraper. All are priced over £50m each. In five years not a single one has sold.

A ‘Shard-shaped disaster’

The key problem with London’s property market is that the developers and government are keen only to serve the tip of the triangle – the wealthiest Brits and international buyers.

But this is no longer where the demand is. Many of those investors from the likes of China and Russia are keen to shift properties they bought a few years ago. Illusions of making quick profit shattered in the wake of the slowing property market and massive currency devaluation of Brexit.

International investors really don’t care where they buy. London is most likely not their home, or where they plan to spend a significant amount of time. They will find the next property bubble or asset class that will serve their millions far better. Where Brexit isn’t a ‘thing’ and stamp duty cannot touch them.

It is the bottom of the Shard that is struggling. The foundations of London’s society. There are no affordable properties being built for those who have to work in London, or at least want to work in London. Estate agent Savills estimates that 58% of demand in London is for homes priced below £450k, but only 25% of homes being built are at this price.

This does not bode well long-term for the UK’s capital. At a time when the Prime Minister and members of the Royal Family are traveling the world in an effort to show the country is open for business, why would a foreign company move to or expand it’s presence? Brexit aside, if employees are unable to find somewhere affordable to live in the capital, businesses will not be tempted to come to an area where they are unable to attract key talent and core workers.

Salesmen begin to suffer

Foxtons is one of the capital’s largest estate agents. Their offices alone have been an excellent marker for the size of the London bubble.

From personal experience I realised we were in full bubble mode when I organised to see a property in South-East London five years ago. I caught the bus there. The estate agent turned up in a brand new Porsche Cayenne.

Source: Guardian

Since then Foxtons capital offices have been transformed into large glass-fronted show spaces, akin to a Scandinavian concept furniture store. They display no properties in the window. Instead there are low coffee tables and armchairs for you to place yourself in as someone greets you and gets you a drink from the moodily lit fridges in the middle of the space.

Eventually someone called Darren in a shiny suit swaggers around and asks you lots of invasive questions about your finances. In no other industry would someone get away with interviewing you like this.

For a long-time Foxtons have survived on the premise that the customer needs them more than they need the customer. Now the tap has run dry and so have their profits.

Last week announced expectations that its earnings before interest, taxes, depreciation and amortisation for the last twelve months to come in at just £15m, a 42% drop from its £26m earnings in 2016. This followed a year of dire financial statements from the company.

It’s not just London estate agents that are suffering. Countrywide, the UK’s largest estate agents have seen their share price fall by nearly a fifth after the group issued its second profit warning in three months.

Much of the group’s disappointing results were thanks to sales in London and the South-East, but data from elsewhere suggests the London-curse is set to spread across the country.

Country-wide properties and buyers are slumping

The Royal Institution of Chartered Surveyors found that 86% of its members surveyed had not seen any increase in inquiries from first-time buyers in December. The same survey found that the number of new buyer inquiries fell last month by 15%. Agreed sales also dropped across the country, with a balance of 13% reporting a decline in volumes.

Investment house, Goodbody took this information and concluded that we are now in ‘the first stage of a housing downturn’.

Data published by HMRC found that the number of homes changing hands in December fell to 99,100, the lowest level since November 2016.

It is clear that the UK property market is stumbling, it is only stumbling now partly thanks to the strong gusts that are coming from the bursting bubble that is London’s property market as people seek alternatives.

The bitter cold of London’s prices will soon sweep around the country and bitcoin mania will no longer be the dinner-party conversation of choice.

Property gold? London property bubble should be a warning to all speculators

For too long the capital has encouraged speculators that prices will continue to rise for ever. As with bitcoin, the capital’s properties became these extreme financial assets that delivered capital gains far in excess of people’s ability to earn income from work, or from investment in the real economy.

For so many government ministers, questioned about the unaffordable London property market they had a two part response. The first was that it was a positive sign for the whole country. The second was that high prices were thanks to too little supply.

Gold in GBP – 10 years (GoldCore)

Really it has nothing to do with a shortage of supply, it has had everything to do with encouraging speculation.

Speculation has been fuelled by governments encouraging home ownership by UK residents and speculation by foreign investors. All of this was further fuelled by record-low interest rates, zero-rate mortgages, loans from the bank of Mum and Dad, government subsidies and tax breaks. It has all been kindling on an ever-growing fire.

Time to diversify and own the physical property of real gold.

Related reading

London Property Crash Looms As Prices Drop To 2 1/2 Year Low

London House Prices Are Falling – Time to Buckle Up

London Property Bubble Bursting? UK In Unchartered Territory On Brexit and Election Mess

Follow Us On Facebook, Linkedin and Twitter

News and Commentary

Gold drops on firmer dollar, higher bond yields (Reuters.com)

Asia Stocks Follow U.S. Drop as Bond Slump Extends (Bloomberg.com)

Stocks Fall as Treasury Yields Climb to 2014 Highs (Bloomberg.com)

These Are The 6 Traders Who Were Just Arrested For Manipulating The Gold Market (ZeroHedge.com)

U.S. Releases Sweeping List of Russian Oligarchs and Officials (Bloomberg.com)

Latest Updates on Russia Sanctions List (Bloomberg.com)

Source: US Treasury via Bloomberg

Gold Prices At Their Highest Since August 2016 (Gold-Eagle.com)

Gross Domestic Problems (MauldinEconomics.com)

This is why – and how – to combat consistency (StansBerryChurcHouse.com)

Davos Dumbbells (BonnerAndPartners.com)

The Donald’s Davos Delusions (DavidStockMansContraCorner.com)

London’s Bankers Haven’t Been This Gloomy Since 2008 (Bloomberg.com)

Gold Prices (LBMA AM)

30 Jan: USD 1,345.70, GBP 954.37 & EUR 1,083.56 per ounce

29 Jan: USD 1,348.40, GBP 955.07 & EUR 1,085.46 per ounce

26 Jan: USD 1,354.35, GBP 950.21 & EUR 1,087.41 per ounce

25 Jan: USD 1,360.25, GBP 954.35 & EUR 1,095.27 per ounce

24 Jan: USD 1,350.50, GBP 957.50 & EUR 1,093.77 per ounce

23 Jan: USD 1,337.10, GBP 959.10 & EUR 1,091.74 per ounce

Silver Prices (LBMA)

30 Jan: USD 17.30, GBP 12.24 & EUR 13.91 per ounce

29 Jan: USD 17.34, GBP 12.33 & EUR 13.99 per ounce

26 Jan: USD 17.40, GBP 12.21 & EUR 13.99 per ounce

25 Jan: USD 17.52, GBP 12.29 & EUR 14.12 per ounce

24 Jan: USD 17.19, GBP 12.16 & EUR 13.93 per ounce

23 Jan: USD 16.98, GBP 12.19 & EUR 13.87 per ounce

Recent Market Updates

– Silver Bullion: Once and Future Money

– Greatest Stock Bubble In History? GoldNomics Podcast Transcript

– Is This The Greatest Stock Market Bubble In History? Goldnomics Podcast

– Government Shutdown Ends – Markets Ignore Looming Debt and Bond Market Threat

– Global Pension Ponzi – Carillion Collapse One Of Many To Come

– The Next Great Bull Market in Gold Has Begun – Rickards

– Gold Bullion May Have Room to Run As Chinese New Year Looms

– Digital Gold Flight To Physical Gold Coins and Bars

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– London Property Crash Looms As Prices Drop To 2 1/2 Year Low

The post London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000 appeared first on GoldCore Gold Bullion Dealer.

![]()

Leave A Comment

You must be logged in to post a comment.